- Wondering if Alphabet is a smart buy at the current price? You’re not alone, especially if you’re trying to spot real value beneath the headlines.

- Despite a choppy recent week with a 2.4% drop, Alphabet shares have rallied 12.2% over the past month and are up a whopping 50.1% so far this year.

- The big stories driving these movements include Alphabet’s continued advances in artificial intelligence and recent antitrust headlines. This has sparked fresh debate about its long-term prospects and is fueling both enthusiasm and caution among investors trying to figure out what the future holds for the company.

- On our 6-point rating scale, Alphabet scores a 3 out of 6 for undervalued, meaning half of the signals suggest its price could be fair or even offer an opportunity. Below, we’ll break down what that really means, and at the end, present a more holistic way to evaluate whether Alphabet is truly a bargain or not.

Alphabet returned 60.3% over the past year. See how this compares to the rest of the interactive media and services industry.

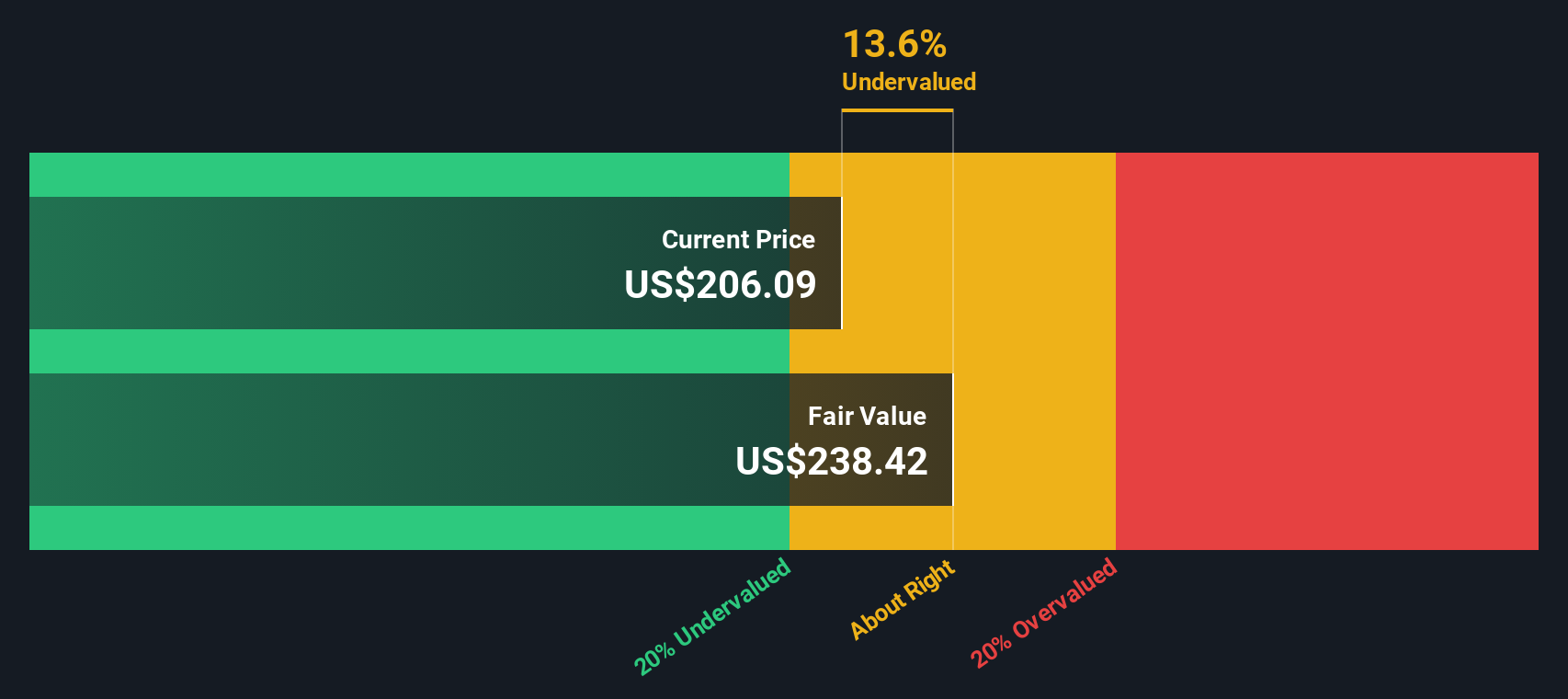

Method 1: Alphabetical Discounted Cash Flow (DCF) Analysis

A discounted cash flow (DCF) model estimates the value of a company by projecting its future cash flows and then discounting them to current dollars. This gives investors an idea of what the company is really worth based on its future earnings potential.

Alphabet’s current free cash flow stands at $92.6 billion. Analysts project this figure will continue to grow, reaching around $157.6 billion in 2029. It is worth noting that while analyst estimates cover the next five years, more forward-looking figures are extrapolated to complete the 10-year outlook. These projections provide a clearer idea of where Alphabet’s underlying business is headed.

Using this approach, the estimated intrinsic value is $285.65 per share. At the current price, this implies that Alphabet is trading at about 0.5% less than its calculated value, making its value quite reasonable by the model’s measure.

Result: ABOUT RIGHT

Alphabet is fairly valued based on our discounted cash flow (DCF), but this can change at any time. Track security in your watchlist or portfolio and receive alerts on when to act.

Head to the Valuation section of our Company Report for more details on how we arrived at this fair value for Alphabet.

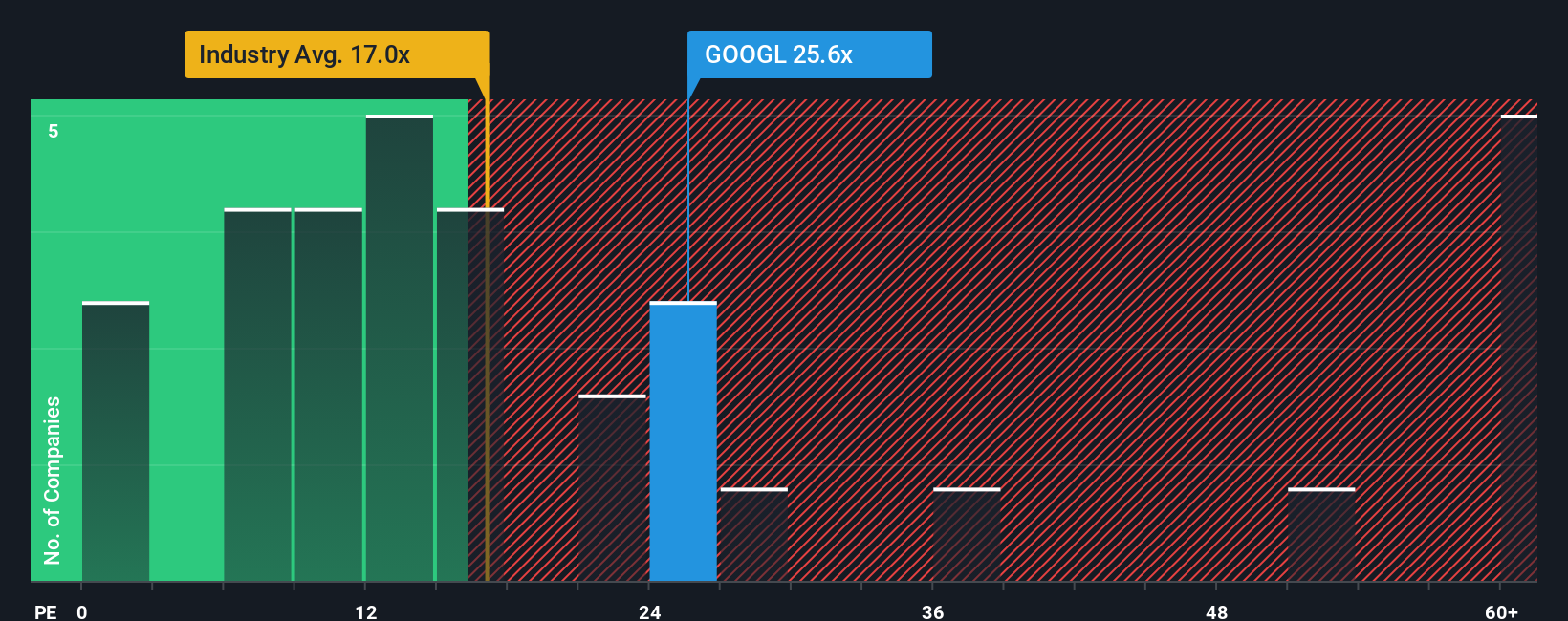

Method 2: Alphabet Price vs Earnings

The price-to-earnings (PE) ratio is widely recognized as the benchmark valuation metric for profitable companies like Alphabet. This ratio tells investors how much they are paying for each dollar of the company’s earnings, offering a quick snapshot of how the market currently values its earnings potential.

The “right” PE ratio for a given company is influenced by a number of factors, such as expected earnings growth, the stability of those earnings, and the inherent risks involved. Greater growth prospects and stronger competitive positioning generally justify a higher PE, while risk or uncertainty would typically reduce that number.

Alphabet’s current PE ratio stands at 27.6x, putting it above the broader interactive media and services industry average of 16.4x, but below its peer average of 36.5x. Simply Wall St’s proprietary Fair Ratio for Alphabet is 40.5x, which incorporates not only traditional benchmarks but also factors such as the company’s profitability, market capitalization, growth rate and risk profile.

The Fair Ratio stands out because it looks beyond a simple comparison between industries or peers and captures nuances such as Alphabet’s exceptional margins, scale and growth profile. This makes it a more tailored benchmark for what a reasonable multiple would look like for Alphabet itself.

With the true PE ratio of 27.6x well below the fair ratio of 40.5x, the data suggests that Alphabet is currently undervalued on this measure.

Result: UNDERVALUED

PE ratios tell a story, but what if the real opportunity lies elsewhere? Discover 1,416 companies where experts are betting big on explosive growth.

Upgrade Your Decision Making: Choose Your Alphabetical Narrative

We mentioned earlier that there’s an even better way to understand valuation, so we introduce you to Narratives, a new approach that connects a company’s history, your expectations for its future (such as revenue, earnings and margins), and your own sense of fair value in a dynamic investing framework.

A narrative is simply your perspective, a story about Alphabet’s future backed by concrete financial assumptions such as growth rates, profitability, and the fair price you believe the stock is worth. The power of narratives is that they allow you to clearly state the because behind your numbers and instantly see how your story translates into potential upsides or downsides based on the current stock price.

Available directly within the Simply Wall St community page and used by millions of investors, narratives help you make more informed decisions by directly comparing your fair value estimate to the current market price, clearly showing when you think it’s time to buy, hold or sell. Better yet, narratives are proactively updated as news, earnings or industry events occur, keeping your investment thesis aligned with reality in real time.

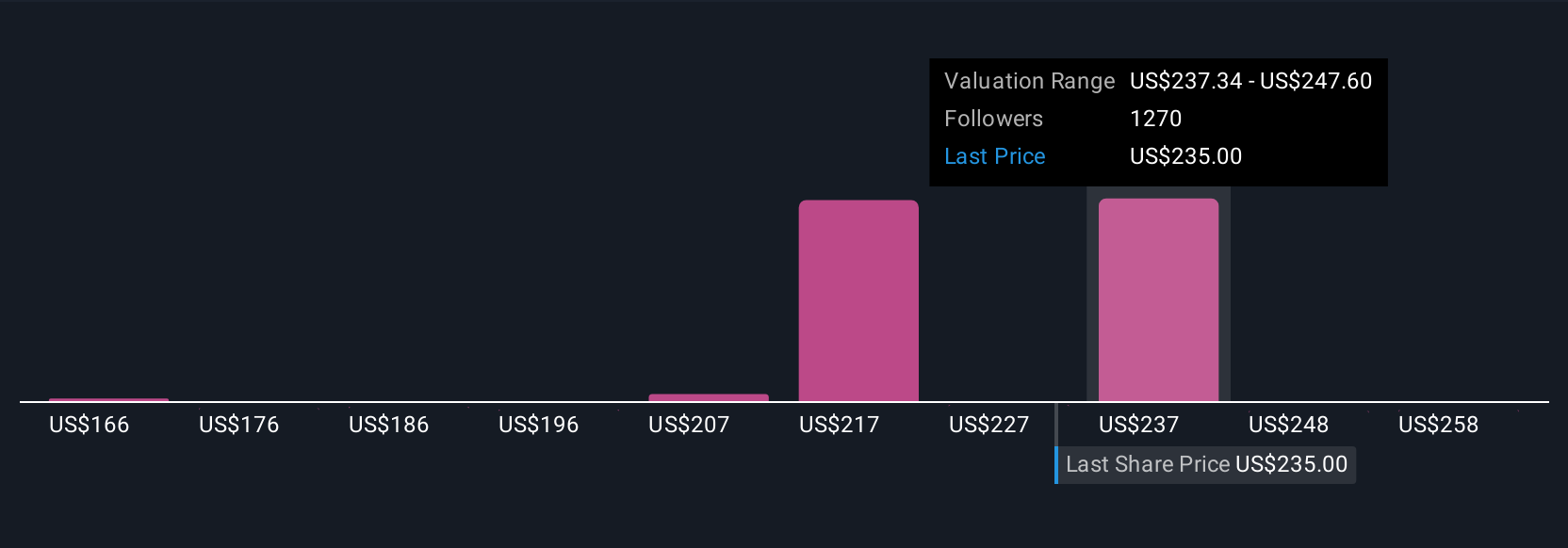

For example, some investors recently valued Alphabet as high as $340 (expecting rapid AI-driven growth and margin expansion), while others see a fair value closer to $171 (anticipating slower revenue growth and slower regulatory impact). Narratives help you place your own vision on this spectrum and update it as the story develops.

For Alphabet, however, we’ll make it very easy with previews of two notable Alphabet narratives:

🐂 Alphabet Bull Case

Fair value estimate: $318.24

Current price vs fair value: 10.7% undervalued

Projected revenue growth: 12.7%

- Analysts see Alphabet’s future profitability driven by growing adoption of AI, innovation in Search and Cloud, and diversification into new global markets and services.

- Strong momentum from AI-based offerings, record growth from Google Cloud, and new subscription models are expected to boost revenue and improve margins. These factors can offset the risks arising from heavy capital spending and a changing regulatory landscape.

- Consensus forecasts indicate steady earnings growth and resilient margins, resulting in a fair valuation near $318. Sustained execution and prudent investment remain crucial for long-term growth.

🐻Alphabet Bear Case

Fair value estimate: $212.34

Current price vs fair value: 33.9% overvalued

Projected revenue growth: 13.5%

- Alphabet’s growth will remain anchored in digital advertising and cloud computing, but monetizing generative AI at scale faces near-term cost and profitability challenges.

- Although Google’s ecosystem and cost initiatives are strong, margins and valuation may be stretched if generative AI expenses remain high and competition in search and AI increases.

- The bear case expects market optimism to come before effective execution and that Alphabet could be at risk of becoming overvalued if disruptive innovation or tighter regulation impacts growth and earnings.

Do you think there is more to the Alphabet story? Head to our community to see what others are saying!

This Simply Wall St article is general in nature. We provide commentary based on historical data and analyst forecasts using only unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell shares and does not take into account your objectives or financial situation. Our goal is to provide you with focused, long-term analysis driven by fundamental data. Please note that our analysis may not take into account the latest announcements from price-sensitive companies or qualitative material. Simply Wall St has no position in any of the stocks mentioned.

New: Manage all your stock portfolios in one place

We have created the ultimate wallet companion for stock investors, and it’s free.

• Connect an unlimited number of wallets and see your total in one currency

• Receive alerts about new warning signs or risks by email or mobile device

• Track the fair value of your shares

Try a free demo wallet

Do you have any comments about this article? Worried about content? Contact us directly. Alternatively, email editorial-team@simplywallst.com