")

Fitch Ratings says oil prices could average around $87 a barrel in 2026 as the reopening of the Strait of Hormuz will reduce global crude supply in the coming months. Despite a sharp rise in prices due to the closure of the key sea route, the global oil market is likely to return to surplus once shipping through the Strait of Hormuz resumes, the report said.“Oil prices would be lower if Hormuz reopens earlier. Uncertainty remains over the timing of Hormuz’s reopening and oil prices will remain volatile as a result,” Fitch says.The rating agency said the disruption resulted from a temporary supply disruption caused by logistics issues rather than a permanent reduction in oil production. “This disruption will not alter the long-term direction of the market, which is expected to return to surplus later this year,” Fitch Ratings said.Under its base-case scenario, Fitch expects the Strait of Hormuz to reopen by the end of July, implying a closure period of about five months. Based on this assumption, the agency estimates the average price of Brent crude to be $87 per barrel in 2026.Read this also Hormuz crisis fallout: How Indian refiners are adjusting new crude oil mix to maximize output

Why is the Strait of Hormuz important?

The Strait of Hormuz remains one of the most important energy transit routes globally, carrying a significant share of worldwide oil exports.

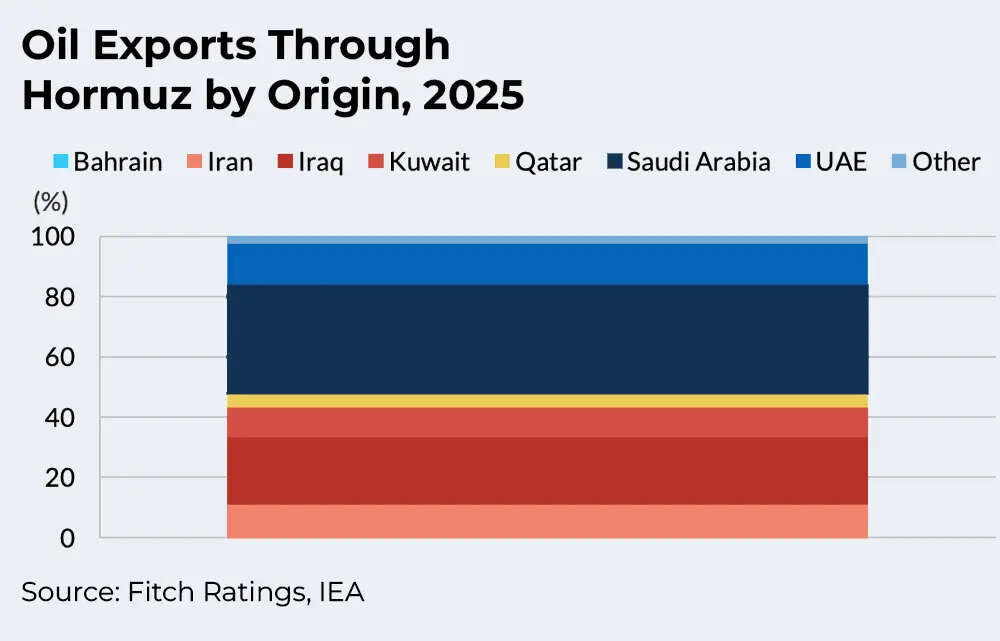

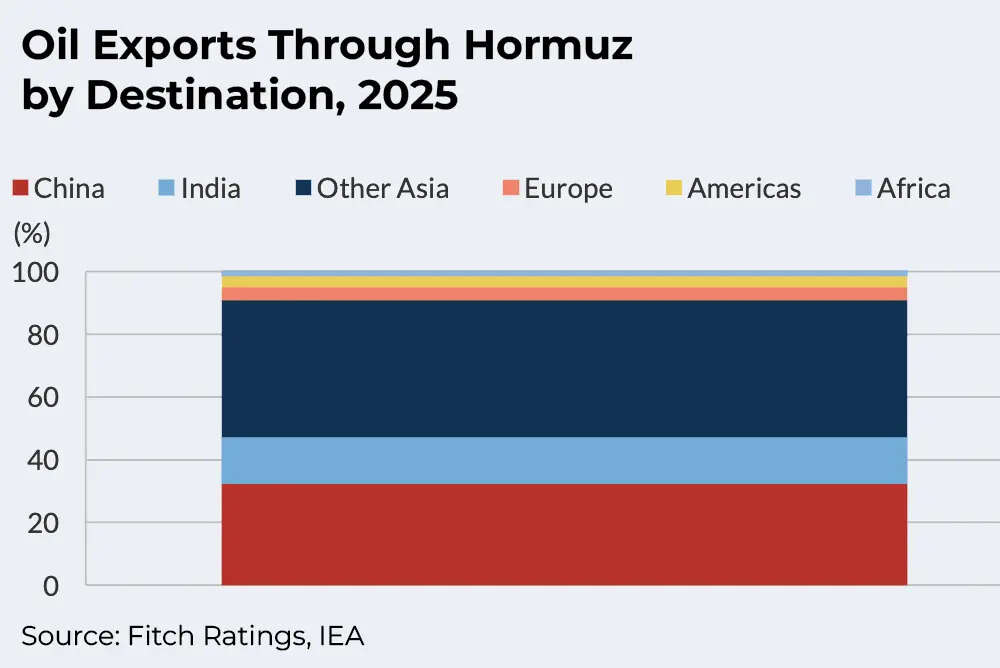

Any disruption to traffic through the strait has major consequences for global energy markets and the broader economy. Before the conflict, about half of the oil transported through the Strait of Hormuz came from Saudi Arabia and the United Arab Emirates. The remaining quantity was exported by Iraq, Kuwait and Iran. China and India together accounted for almost half of the destination demand for these shipments.Fitch said the recent surge in oil prices reflects a short-term logistics disruption rather than a permanent loss of production capacity, and expects Brent crude to fall sharply once normal shipping operations resume.The agency estimates that global oil markets will return to an oversupplied situation by September. This outlook is supported by the rapid recovery in West Asian oil production, strong supply growth from non-OPEC producers and the possibility of OPEC increasing output beyond pre-conflict production levels.

No major damage to infrastructure

So far there has been no significant damage to the oil infrastructure. The report said that past experience also shows that the restoration work can be completed relatively quickly. Following the 2019 attacks on its facilities, Saudi Aramco was able to make repairs and resume operations within approximately two weeks.Given the limited impact on regional oil infrastructure to date, production is expected to increase rapidly throughout the Middle East. When shipping resumes, oil already in tankers and onshore storage facilities is likely to reach the market first, followed by the resumption of previously reduced production.Before the conflict, 91% of the crude oil transported through the Strait of Hormuz came from Asia, with China receiving 32% and India 15%. As a result, Asian markets have borne the brunt of the petrochemical sector’s response to the disruption.